How Medical Insurance works in USA: A Guide for Russian Speakers

For over 12 years, I’ve helped more than 1,300 Russian-speaking clients understand U.S. health insurance. Many of them say the same thing:

“I don’t understand how Obamacare works, and I don’t want to get ripped off.”

If you’ve ever felt the same, this article will help. I’ll walk you through real costs, show you how to compare plans, and explain how to avoid common mistakes—based on real experiences with hundreds of clients.

What the Affordable Care Act Did—and Still Does

The Affordable Care Act (ACA), also known as Obamacare, reshaped U.S. health insurance . Before 2010, millions lacked coverage. Some couldn’t afford it. Others didn’t have access through their employers.

The ACA introduced major changes:

- Health insurance marketplaces like Healthcare.gov

- Subsidies that reduce monthly premiums based on income

- Protections for people with pre-existing conditions

- Medicaid expansion in many states

A Quick History of U.S. Health Insurance

Understanding today’s system means looking at how it developed:

- Late 1800s: Companies offered basic accident coverage to workers

- Mid-1900s: Employers began offering full health insurance benefits

- 1990s: New laws allowed small businesses to cover chronic conditions

- 2010s: The ACA made individual plans more accessible and added stronger protections

Each step responded to economic changes, public health crises, and political pressure. The system grew piece by piece.

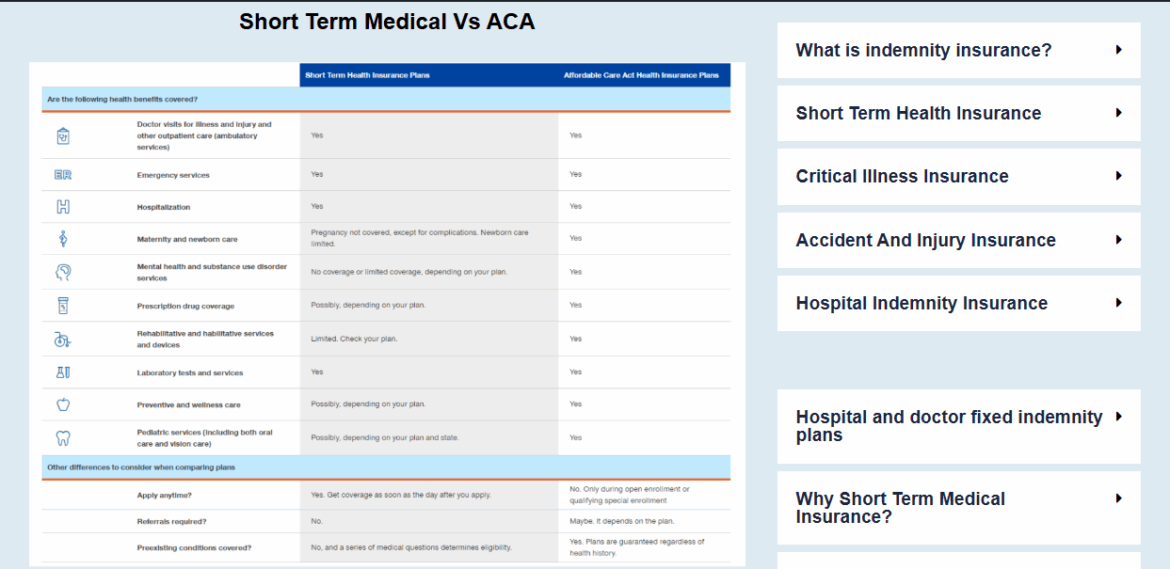

Obamacare vs. Trumpcare: What Changed?

When President Trump took office, he didn’t eliminate Obamacare but made key adjustments:

- He removed the tax penalty for not having insurance (effective 2019)

- He expanded access to short-term, lower-cost plans for healthy individuals

- He gave more flexibility for people to choose non-ACA plans

For example, a healthy 50-year-old might pay $500–600 per month for an ACA plan but only $150–180 per month for a short-term plan—depending on coverage.

These changes gave more affordable options to people who don’t use medical services often.

Health Insurance Help in Russian

For many immigrants, health insurance feels overwhelming—even native English speakers get confused.

That’s why I help clients in both Russian and English. I explain what each plan covers, how much it costs, and how to choose what fits your life.

I regularly help:

- Self-employed professionals

- Families and new immigrants

- Small business owner

Understanding your plan makes all the difference—especially when medical bills can pile up fast.

Family Health Insurance

Quick Takeaways

Here are key tips to keep in mind:

- Check for subsidies every year—even if you didn’t qualify last time

- Review your plan annually—prices and coverage change often

- Ask questions—guessing usually leads to expensive mistakes

Common Questions Russian-Speaking Clients Ask Me

Q: What’s the best plan for my family?

A: That depends on your income, age, household size, and zip code. I compare options in real-time so you can make an informed choice.

Q: What if I’m undocumented or new to the U.S.?

A: Some states, like New York, offer local programs. I’ve helped green card holders and undocumented workers get basic coverage legally.

Q: Can I get help in Russian?

A: Absolutely. I speak fluent Russian and explain everything clearly—no jargon, no confusion.

I’ll guide you step by step—in Russian or English—so you understand your choices. We’ll find the right plan without the stress or guesswork.

Call or text me directly at 215-690-5006.

You don’t need to overpay. And you don’t need to face this alone.